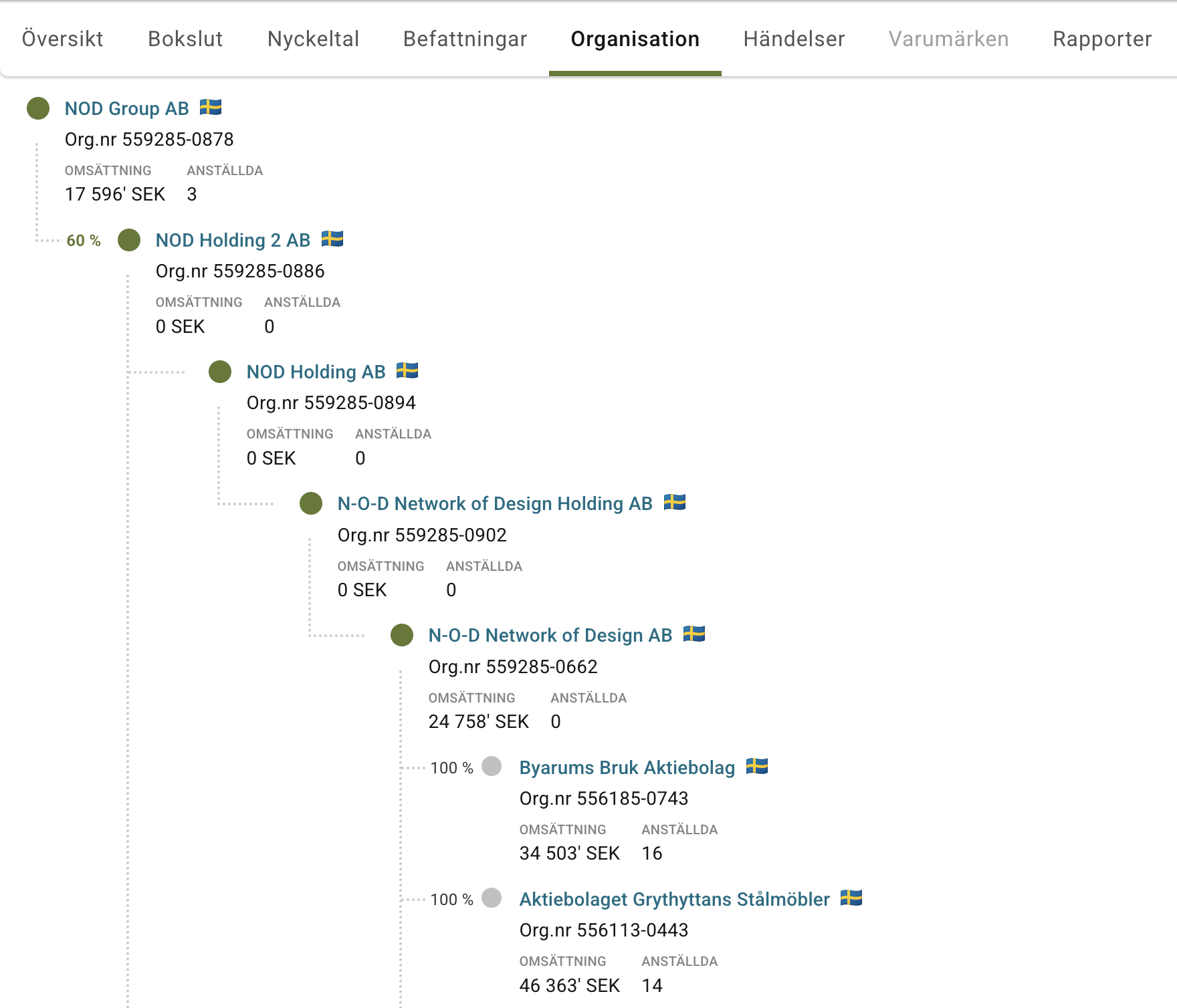

Perché un’azienda dovrebbe essere creata con così tante società di partecipazione?

https://i.redd.it/qz1ez0de26je1.png

di questions123abc

Perché un’azienda dovrebbe essere creata con così tante società di partecipazione?

https://i.redd.it/qz1ez0de26je1.png

di questions123abc

7 commenti

5:25

Förmodligen skattefiffel

Bara för att fiffla med stålar. Med tanke på deras verksamhet.

When a limited liability company (“daughter company”) is sold by another LLC (“mother company”) the compensation is tax exempt before being transferred to the sellers owners (dividend). Swedish tax rules stipulates an effective tax cut when a company, LLC, has been “laid to rest” wothout being liquidated for a period of five years (if that company is owned by someone who works in that same company and the company does not employ to many other people). Meaning if I wait 5 years before liquidation after effectively dismantling my company and lifting only a modest sum each year as dividend – I effectively dodge a large portion of tax. 25% tax rather than almost 50%, if enough profits, is preferable for most LLC sellers.

This type of situation is most often related to retirement.

What appears to be the case in OP’s picture is a company which has undergone this procedure multiple times. The original company was bought by a holding company who later sold its shares to another holding company for tax “evasion” (perfectly legal) purposes. This process was later done again. And so forth until it had this many holding companies.

Inte nödvändigtvis fiffel. Det är enklare för att hantera olika ägarskap samt försäljning.

Utöver bolaget kanske du har en koncern ovan som samlar gemensamma funktioner och kostnader. Koncernen ägs sedan av ett holdingbolag som gör det enkelt att ge aktier till chefer eller anställda i incentivprogram utan full insyn/kontroll i koncernen, dvs rent ”ägarskap”. Holdingbolaget ovan kan ge möjlighet att sälja bolaget (från incentiv holding och nedåt) utan att behöva ”karva ut” det ur ett bolag som äger många bolag. Och sen har du det faktiska stora ägarbolaget på toppen.

Det är ju såklart Brotherhood of NOD som behöver finansiera Kane’s planer!

Fred genom makt!

Jag ska lägga på minet “Grythyttan Stålmöbel” som namn till nästa DnD orken, tack för det.